Exam 1 study guide

Capitalism + governments and institutions

You should understand…

- …the components of the capitalist economic system: private property, markets, and firms

- …what happens when any of these components gets distorted

- …what makes public goods different from regular goods (see public goods game)

- …what institutions are and how they coordinate action

- …what GDP is, what it measures, what it doesn’t measure, what problems there are with it, what alternatives there are for it, and why it continues to be popular

- …the difference between real and nominal values (and why we care)

- …what a price index is

- …what purchasing power parity (PPP) is (and also what the Big Mac Index is)

- …the downsides of capitalism (inequality + environmental damage)

- …why not everything should be a market

- …why large groups suffer from free riding and how they work to behave like small groups

- …how small factions threaten democracy, but also how they enable it

- …how voting can suffer from failures (Condorcet’s paradox)

Important formulas:

Adjusting for inflation:

\[ \text{Real} = \frac{\text{Nominal}}{\text{Price Index / 100}} \]

Percent change:

\[ \text{% change} = \frac{\text{New} - \text{Old}}{\text{Old}} \]

or

\[ \text{% change} = \frac{\text{Current} - \text{Previous}}{\text{Previous}} \]

Compound annual growth rate (CAGR); periodic method (this assumes interest is compounded once a year; this is the harder method and you don’t really need to use it):

\[ r = \exp(\frac{\ln(\frac{\text{Price index}_{\text{new}}}{\text{Price index}_{\text{old}}})}{t}) - 1 \]

Compound annual growth rate (CAGR): continuous method (this assumes interest is compounded continuously; this is the easier method and you should generally use this):

\[ r = \frac{\ln(\frac{\text{Price index}_{\text{new}}}{\text{Price index}_{\text{old}}})}{t} \]

Guides:

Other helpful resources:

Fairness and efficiency

You should understand…

- …the difference between Pareto efficiency and fairness

- …why Pareto efficiency is not necessarily the best standard for measuring the success of a policy

- …how we can measure fairness with substantive standards, procedural standards, and Rawlsian standards

- …how cultural perceptions of luck and fairness shape public policy

- …how ideas of efficiency and fairness apply to international trade

- …how public policy can be used to change the payoffs in games (e.g. making it more expensive to use water and deplete public goods)

- …what elasticity measures (i.e. what it means for something to be inelastic vs. elastic)

- …why good public policies should be a Nash equilibrium

- …the difference between absolute and comparative advantage and how there can still be gains from trade if a part doesn’t have absolute advantage in a product

Guides:

Work, wellbeing, and scarcity

You should understand…

- …what opportunity costs are and how they influence decision making

- …how to draw a budget line and what budget lines mean

- …how utility is measured and what indifference curves are

- …the difference between the marginal rate of substitution (slope of the indifference curve) and the marginal rate of transformation (slope of the feasible frontier)

- …what it means when marginal product and marginal utility diminish

- …how to find the utility-maximizing level of consumption given preferences and budget constraints

- …the difference between normal and inferior goods

- …what income effects and substitution effects are and how they’re related to government policies

Important formulas:

All the ways marginal utility (or marginal rate of substitution) can be written:

\[ MRS = \frac{dy}{dx} = \frac{\Delta y}{\Delta x} = \frac{\text{Price}_x}{\text{Price}_y} = \frac{MU_x}{MU_y} = \frac{\partial u / \partial x}{\partial u / \partial y} \]

Guides:

Other helpful resources:

- How to draw income and substitution effects

- Example Income and Subsitution Effects For Normal and Inferior Goods

- Income and Substitution Effects

The firm

You should understand…

- …how the decision-making structures of firms and markets are different

- …that perfectly complete contracts are difficult (if not impossible) to create

- …what happens when there are incomplete contracts

- …what a principal-agent problem is

- …adverse selection

- …moral hazard

- …how firms can use the labor discipline model to induce higher worker effort

- …why involuntary unemployment is necessary

Firms and markets

You should understand…

- …how demand curves are derived from consumer willingness to pay

- …the difference between fixed costs and variable costs

- …how to calculate total cost, total revenue, average fixed costs, average variable costs, marginal cost, marginal revenue, and maximum profit

- …that maximum profit occurs where marginal revenue is equal to marginal cost (\(MR = MC\))

- …that socially optimal quantity occurs when the demand is equal to the marginal cost (\(\text{demand} = MC\))

- …how to calculate elasticity of demand (\(-\frac{\Delta Q}{\Delta P} \times \frac{P}{Q}\))

- …what elasticity measures and why it is important in public policy and administration

- …how a single demand curve can have an overall elasticity and different elasticities at each point

- …economies of scale, diseconomies of scale, economies of agglomeration, network effects, and the difference between short-run and long-run costs

- …that market equilibria (i.e. optimal price and quantity) occur at the intersection of supply and demand curves

- …how government-imposed price floors and price ceilings distort market-clearing equilibria

- …and be able to identify the differences between changes in supply/demand and changes in quantity supplied/demanded

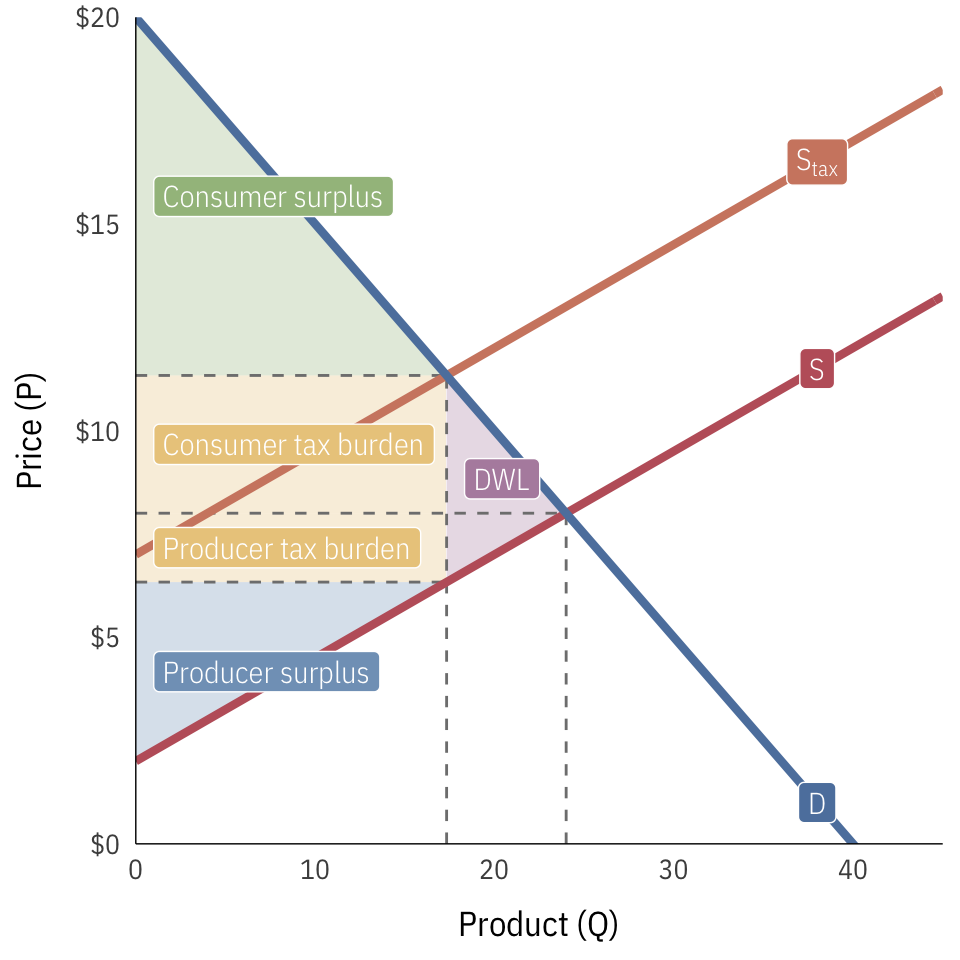

- …what consumer and producer surplus represent

- …the relationship between elasticity of supply and/or demand and the size of consumer and producer surplus

- …how taxes impose deadweight loss on society

- …how the burden of taxes depends on the elasticity of supply and/or demand

- …why governments tax and the philosophical and ethical principles behind who should bear the burden of taxes

- …the difference between price-taking and price-making

- …how firms try to gain market power, including monopolies, branding, cost controls, regulation, and switching costs

- …why firms try to gain market power

- …why firms want to price discriminate

- …the consequences of monopolistic production (lower Q and higher P than what would happen under perfect competition; deadweight loss)

- …how governments can regulate monopolies

- …why natural monopolies exist and how governments can induce them to produce at socially optimal levels

- …how firms need to be somewhat anti-competitive and anti-capitalist in order to maximize profits, innovate, and (essentially) be more competitive and capitalist

Guides

Important formulas:

Demand:

\[ P = aQ + b \]

Total cost:

\[ \begin{aligned} TC = TFC + TVC \\ \text{or a formula using } Q \text{, like} \\ TC = aQ^2 + b \end{aligned} \]

Average cost:

\[ AC = \frac{TC}{Q} \]

Marginal cost:

\[ \begin{aligned} MC &= \frac{\Delta TC}{\Delta Q} \\ &\text{or} \\ MC &= \text{First derivative of TC} \\ &= 2aQ \text{ (if } TC = aQ^2 + b) \end{aligned} \]

Total revenue:

\[ \begin{aligned} TR &= PQ \\ &\text{or} \\ TR &= (aQ + b)Q \\ &= aQ^2 + bQ \end{aligned} \]

Average revenue:

\[ AR = \frac{TR}{Q} \]

Marginal revenue:

\[ \begin{aligned} MR &= \frac{\Delta TR}{\Delta Q} \\ &\text{or} \\ MR &= \text{First derivative of TR} \\ &= 2aQ + b \text{ (if } TR = aQ^2 + bQ) \end{aligned} \]

Maximum profit:

\[ max(\pi): MC = MR \]

Price elasticity of demand (see this guide of how to get to \(- \frac{\Delta Q}{\Delta P} \times \frac{P}{Q}\)):

\[ \varepsilon = -\frac{\% \text{ change in quantity demand}}{\% \text{ change in price}} = - \frac{\Delta Q}{\Delta P} \times \frac{P}{Q} \]

Important graphs:

Consumer surplus, producer surplus, tax revenues, tax burdens, and deadweight loss (use algebra and geometry to figure out the areas of the triangles (\(\frac{1}{2} \times b \times h\)) and rectangles (\(l \times w\))):

Helpful resources:

- Derivatives of Exponential Functions (how to calculate derivatives quickly)

- Jason Welker, “Natural Monopoly and the Need for Government Regulation”

Social interactions, economic outcomes, and incentives

You should understand…

Guides:

Other helpful resources: